If you are fairly well versed in finance, you may know that exchange-traded funds (ETFs) are tax-efficient, but can you explain why? Mutual funds and ETFs are cut from the same cloth, but they carry distinct differences in how they are traded, created, and redeemed. These differences all add up to make ETFs more tax-efficient. Here, we’ll explore how and why this can save you money in the long run.

Understanding the Difference Between ETFs and Mutual Funds

On paper, ETFs and mutual funds are very similar. They’re practically investment cousins.

But what makes ETFs more tax efficient has more to do with how they are built, their creation-and-redemption mechanism, and how frequently they turnover. This accumulation of features makes them great for taxable accounts.

Mutual Fund Basics

Mutual funds are pretty straightforward. Investors pool together their cash, then give the money to a portfolio manager who purchases assets (stocks and bonds typically). Investors can contribute more money to buy more stocks or free up cash by selling current holdings to buy new stocks. Mutual funds generally grant access to a broader range of stocks than you could afford on your own.

A mutual fund can follow major indexes, like the S&P 500, or the manager can compile a custom group of stocks. Mutual funds are only traded once a day at the end of the day. Any dividend distributions or capital gains from shares sold are distributed as cash among the shareholders, and these distributions are taxable. Shareholders also bear the burden of any fees or trading costs.

When mutual funds are held in retirement accounts, like a Roth IRA or Traditional IRA or 401(k), they will retain the tax benefits of that account. For example, tax-deferred funds remain tax-deferred even in a mutual fund. If you’re looking for a tax-efficient taxable account, ETFs are a better option.

Anatomy of an ETF’s Tax Efficiency

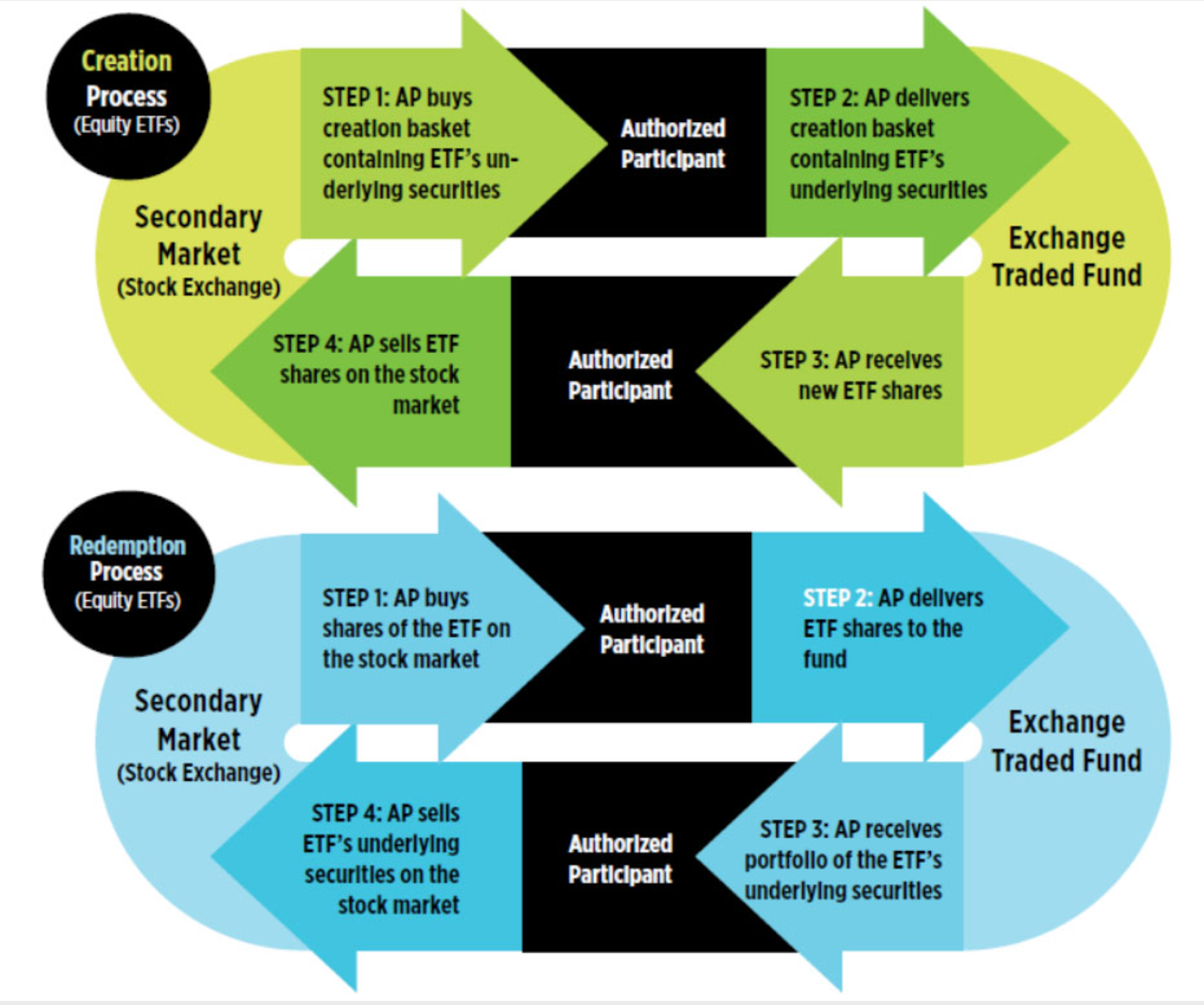

To create an ETF, an authorized participant (AP) will purchase a block of stocks to form what is called a creation unit. This process is regulated by the SEC (Securities and Exchange Commission). Since these blocks are generally made up of 50,000 shares, APs have a lot of buying power, and average investors are unable to create ETFs on their own.

The AP will then sell shares of the ETF and manage the fund to ensure its net asset value (NAV) and the market price of the shares or index it follows are near equal. The AP also shoulders the weight of the fund, such as trading costs and fees.

Shares are added or sold through a distinctive creation-and-redemption mechanism that reduces the impact and frequency of gains from ETFs. Shares within mutual funds are bought and sold, but ETFs can create in-kind sales, which means securities are traded for other securities. Transactions stay within the stock exchange and don’t trigger capital gains as often.

ETF Creation/Redemption Mechanism

Photo credit: ETF.com

When ETFs distribute capital gains, it’s usually much less frequently and for smaller amounts. A recent Morningstar contributor put together a mockup of the capital gains earned between an ETF and mutual fund with the same stocks. Over a 10-year period, mutual investors paid more, and more often than ETF investors.

As a passive investment tracking an index, ETFs typically have a lower turnover. Investors tend to invest and leave the funds for the AP or fund manager to maintain.

ETFs Aren’t Tax-Immune

All of this talk about tax efficiency may make it seem like ETFs are tax-free investment accounts. After all, their efficiency is derived from generating fewer taxable events-like capital gains-than mutual funds. However, these events still happen, and you’ll still need to pay taxes on any earnings. And, of course, dividends from stocks and interest from bonds are still taxable.

A Word About NAV and Bid/Ask Spreads

Critics of ETFs will often cite NAV and bid/ask spreads—elements of the creation/redemption process that makes ETFs tax efficient—as reasons to be cautious or at least attentive.

When an ETF is created, it’s given a net asset value (NAV) that represents the overall value of the shares within the fund. This is NOT the market price of the fund.

To keep it simple, let’s say an ETF is made up of Security A and Security B.

- Security A = $1

- Security B = $1

You’d assume that ETF’s NAV is $2, but in reality, it will fluctuate around $1.98 or $2.02. A fund’s NAV is one half of the scale an ETF sponsor must maintain between the value of the ETF and the value of securities or shares within the fund.

If the scale tips toward the NAV, the ETF may be more valuable than the shares it represents. The ETF sponsor will then sell or redeem ETF shares to lower the price and bring it more in line. If the scale tips toward the value of the securities, the more shares of the ETF are created to increase the NAV.

This balancing act could be risky for ETF investors if the bid/ask spread is too wide. A bid/ask spread is simply the difference between the price a seller is willing to offer (supply) and how much a new buyer is willing to pay (demand). If the spread is too wide—like during a high liquidity market—or not properly maintained by the creation/redemption mechanism, investors could lose money.

Other Benefits of ETFs

For new investors or investors looking to diversify their portfolios, ETFs offer other non-tax benefits.

One major benefit to ETFs is that they are often less expensive than mutual funds. ETFs also require fewer management fees; more specifically, they don’t charge 12b-1 fees. 12b-1 fees are annual marketing expenses, most often paid out in commissions, that many mutual fund companies incur and ultimately pass off to investors. This isn’t an issue with ETFs because there is no need to pay for such operational expenses.

Lastly, ETFs have lower expense ratios. Expense ratios are expressed in percentages and represent how much of a fund’s assets are used for administrative and other operating expenses. This is calculated by dividing the fund’s operating expenses by the amount of funds under management (AUM). Since most ETFs are passive, they’re more likely to have a lower ratio- or sometimes even 0 percent!

Bottom Line

While mutual funds and ETFs have a lot in common, and both can be great options for investment, the key takeaways when comparing the two boil down to:

- Distinctive features make ETFs a more tax-efficient taxable account.

- An ETF’s structure and trading mechanisms protect investors and limit the frequency and impact of capital gains.

- Mutual funds are great vessels for retirement accounts when that account can reduce the tax implications inherent with mutual funds.

- In truth, a strategic combination of ETFs and mutual funds will help you diversify and strengthen your investment portfolio.

No matter what route you take, the goals are simple. You always want to maximize your portfolio’s tax efficiency and keep more money in your pocket and working for you.

Creating a portfolio that’s diversified, efficient, personalized, and growing can be a full-time job. Save yourself time and money from investment mishaps by working with a professional financial advisor at Metanoia Financial. We offer free consultations to help you get started.

Schedule yours today!